What makes Musk’s business model turn technological ambition into record-breaking value? And what does this phenomenon tell us about an economy where hopes for the future increasingly outweigh profits “here and now”?

Photo: nasdaq.com

June 2026 will go down in world economic history as the moment the first dollar trillionaire appeared. After SpaceX’s IPO, Elon Musk’s fortune surpassed the $1 trillion mark. Just ten years ago, such figures seemed like science fiction. But this is not only about a personal record. For the first time, the world’s largest fortune was made not in industry or finance, but at the intersection of private space, AI, and digital infrastructure.

This is an important signal about which industries and ideas are considered the most promising today. Musk’s wealth reflects not so much the financial performance of his companies as investors’ expectations. The market values not only what is already working, but also what may emerge: autonomous transport, neural interfaces, and space expansion.

Why Musk Is Different

The Musk phenomenon is difficult to explain in the usual categories of big business. He is not the heir to a family industrial empire, and he did not build his fortune around a single product or market. His model is more like a group of assets operating in different sectors but united by a common technological logic.

As noted by experts at Harvard Business Review, Musk’s companies are united by a shared vision and approach: he chooses tasks that require overcoming complexity and achieving scale (for example, mass-producing electric vehicles or creating reusable rockets) rather than staying within the traditional boundaries of an industry or product. Organizationally, Musk prefers vertical integration and closed technological systems, which allows him to control the entire value chain and mobilize resources to achieve ambitious goals without becoming dependent on external suppliers or standard market mechanisms.

At first glance, Tesla, SpaceX, xAI, Neuralink, and the X platform are only loosely connected: electric vehicles, space, AI, neurotechnology, and social media are different niches. Yet in Musk’s view, they are all elements of a broader (and seemingly carefully planned in advance) project. This is the key difference between Musk and most of today’s leaders in the Forbes and Bloomberg rankings. The success stories of Big Tech players are stories of many different projects, but ones that grew gradually around a single dominant business. Musk’s empire, by contrast, rests on several directions that reinforce one another, but the links between them are not always immediately intuitive.

This model reflects a major shift in the modern economy: the market value of technology companies is now formed not only by current results, but also by the future scenarios they offer. High valuations for Tesla, SpaceX, or xAI are largely based on the assumption that their technologies will define the future of transport, communications, and, of course, AI.

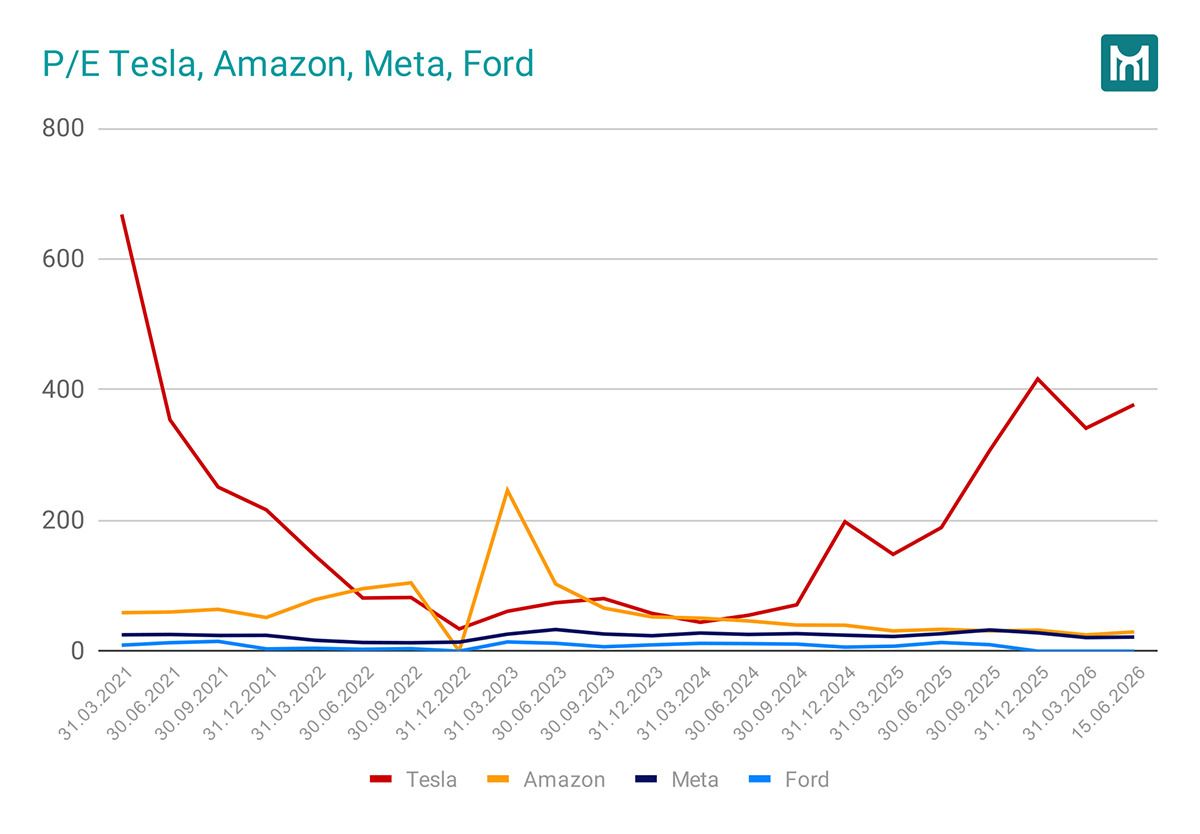

Musk has become one of the visionaries of an economy in which capital concentrates around long-term bets on technology, and the ability to shape an image of the future becomes an asset no less important than production capacity or current profit. When, for example, Tesla trades at a P/E ratio (the ratio of a stock’s market price to earnings per share) above 300, it means investors are not buying into the company because of car sales figures, but rather a stake in the coming revolution in autonomous transport and Optimus humanoid robots.

Source: Macrotrends.net

Nevertheless, Elon Musk’s figure cannot be assessed in isolation from other billionaires. Most leaders of the modern digital economy, as noted above, built their fortunes around one key business: Jeff Bezos created a global e-commerce infrastructure; Larry Page and Sergey Brin turned search and advertising into the foundation of the largest internet ecosystem; Larry Ellison bet on enterprise software — while Mark Zuckerberg monetized social networks and digital attention.

Musk, meanwhile, is steadily building a system in which different companies can complement one another technologically and financially.

The composition of his assets is also striking. Musk’s business combines software and consumer products with “heavy” physical infrastructure (far beyond computers and gadgets): Tesla factories, SpaceX rockets, and Starlink satellites. This shapes government customers’ interest in Musk’s developments — and also their dependence on projects such as NASA and regulators.

In addition, Musk has effectively made his personal brand a standalone asset. While many top executives of his level prefer limited public exposure, Musk has made his own media activity part of his business strategy. His statements regularly spark debate — and often directly affect the value of his companies.

Why Is Musk Building Everything at Once?

The capital sources of the biggest technology players largely determine their strategies. Alphabet, Oracle, and Meta “rose” on the back of revenue from advertising, software, and cloud services — and these remain the foundation of their capital. New projects grow around existing ones and usually do not extend far beyond them.

Elon Musk’s approach works differently. His companies operate not as a set of independent assets, but as elements of a single technological system. AI development within xAI potentially complements Tesla’s autonomous systems, the Starlink satellite network provides global connectivity, and Neuralink explores new forms of interaction between humans and machines. Despite the differences among these projects, they are united by a common vision of the future, in which AI, robotics, and space are tightly intertwined.

From the perspective of traditional management, this is an unusual structure: corporations generally seek to reduce risk by shedding non-core and “unpromising” assets. For example, Meta, like other players, invests in AI — but the high-profile Metaverse project is already forgotten, and the company is steadily winding down the products built around it: that “future scenario” was not believed in — and Meta is moving on to another one, in which other players are already succeeding.

Musk, by contrast, is creating a technology ecosystem designed for decades ahead. This strategy largely explains the scale of his success — but it also implies a high level of risk for his business empire.

The idea of buying SpaceX shares entails many risks for investors, Reuters summarizes expert comments gathered in connection with the IPO; the most notable elements of the “adverse combination of financial and governance risk” are weak corporate governance under Musk’s absolute control, loss-making operations, transactions between his companies, and hard-to-achieve goals such as colonizing Mars and placing data centers in space. Morningstar analysts also pointed to the large number of risks when estimating SpaceX’s fair value at $780 billion. However, as noted in the Reuters piece, “in the scramble to get a piece of the action, few are focusing” on the risks — and everything suggests that demand for SpaceX shares will be high.

How SpaceX Changed the Space Industry

In the early 2000s, the idea that private business could seriously compete with NASA or a Russian Roscosmos was met with skepticism. Musk’s projects were seen as a risky attempt to enter the industry. “I had so many people try to talk me out of starting a rocket company, it was crazy. One good friend of mine collected a whole series of videos of rockets blowing up and made me watch those. He just didn’t want me to lose all my money”, Musk himself recalled. SpaceX’s first three launches failed, and he viewed the successful fourth one (2008) as a gift of fate and a breakthrough.

In the end, however, SpaceX established itself in the market and even became dominant in commercial launches. The key turning point came after the introduction of reusable rockets. Falcon 9’s returnable stages significantly changed launch economics, lowering the cost of placing payloads into orbit. And institutionally, NASA and other customers now critically depend on SpaceX infrastructure: today the company provides crewed missions to the ISS and remains the main contractor in the program to return humans to the Moon, where its next-generation system has already become a basic element of future missions.

At the same time, SpaceX formed a second, no less significant sphere of influence — the Starlink satellite network, “growing” a standard internet service into a global infrastructure platform. Now Starlink is used in maritime logistics, aviation, and remote regions; it has effectively become part of basic digital infrastructure — like traditional backbone networks. In addition, since 2022 Ukraine has received tens of thousands of Starlink terminals, initially thanks to SpaceX and donors (including Poland), and since mid-2023 under contracts with the Pentagon and the U.S. State Department, including the specialized military version Starshield and allocation of $150 million to expand terminal infrastructure.

SpaceX’s commercial direction has also intersected with the U.S. defense sector. The company’s solutions were integrated into military communications and surveillance architecture, and subsidiary programs received major government contracts. This cemented SpaceX’s status as a strategic U.S. partner in space.

Against this backdrop, traditional industry players such as Boeing and Lockheed Martin look less flexible and weaker in terms of resource scale. China’s space program remains the only comparable competitor — though even there, they are still only reacting to changes rather than shaping them.

As a result, SpaceX has transformed from simply a successful business into a structural element of U.S. space infrastructure on which civilian and defense programs depend.

When Business Becomes Politics

In the traditional model, billionaires influence politics through lobbying and donations. Musk has shifted these boundaries by using personal assets as levers of pressure. His path into power is a story of how private interest and the government agenda merged into one with minimal checks and balances.

The $44 billion purchase of Twitter in 2022 became a point of no return. Renaming the platform X (incidentally, this was originally the name of the banking platform founded by Musk banking platform, which became PayPal in 2001), he bet on the removal of moderation. According to a recent study, X’s algorithms deliberately promote right-wing political content: an experiment showed that switching to the algorithmic feed shifts users’ views in a conservative direction — specifically, shaping the opinion that the investigations into Donald Trump were “unacceptable”. Researchers at Germany’s Weizenbaum Institute describe Musk as “The Great SysOp,” a system administrator who manages the network through personal and ideological edits, implementing the concept of “platform illiberalism”. Under Musk’s leadership, the platform has become not just a communication tool, but an active agent of political influence: the reach of hate-inciting tweets is growing, and offending accounts are not blocked, only stripped of monetization.

The culmination of this “entry into power” was the creation of the Department of Government Efficiency (DOGE) after Trump’s victory in 2024, where Musk received the role of “special government employee”. Officially, DOGE was meant to fight bureaucracy, but in practice it led to a concentration of power. Studies show that DOGE used access to critical systems (the Treasury, OPM — the U.S. Office of Personnel Management) to centralize control and dismiss professionals. Scandals followed one after another:

Ethical violations: House Democrats launched an investigation into Musk’s use of DOGE to roll back regulatory acts affecting his own companies (SpaceX, Tesla), which is classified as a “rampant conflict of interest”.

Direct abuses: cases were recorded in which Trump administration officials promoted Tesla stock live on air (by then the company was losing market capitalization) in order to support Musk, which prompted lawsuits over violations of public service ethics.

Layoffs and pressure: under Musk’s leadership, about 200,000 federal employees were dismissed — with wages and benefits preserved until the end of the fiscal year, which cost the budget $14.8 billion. At the same time, the IRS lost key auditors, causing tax return processing to stall and revenue collection to decline.

Musk left DOGE in May 2025 after a public falling-out with Trump (Trump called him “crazy” — Musk threatened him with impeachment). However, his influence did not disappear — the “hybrid leader” format became established. Musk remains the largest political donor (he spent $300 million on the 2024 campaign) and the owner of infrastructure where the agenda is formed. He is less and less an entrepreneur and more and more — in the eyes of his critics — “a techno-populist” who speaks of saving democracy, but in practice is building digital authoritarianism.

Vulnerabilities of the Empire

Even against the backdrop of the historically high valuation of his wealth and influence, Musk’s asset structure remains sensitive to external shocks. His business model relies on high expectations of future growth — which makes it scalable and vulnerable to a simultaneous revision of those expectations. What exactly belongs on the list of risks for Musk’s business?

Musk “sells” the market expectations of the future — but he himself depends on how much people believe in those expectations. A substantial part of his companies’ capitalization rests not on current profits, but on advances: investors pay for promised breakthroughs — robotaxis, autopilot, colonizing Mars — and as long as belief remains strong, the stocks rise. But once the market begins to doubt that miracles are coming, or simply shifts attention to other stories, the fragility of such a model becomes obvious. Technology bubbles burst in exactly this way: not because of bad reports, but when investors grow tired of waiting. In the event of a sector correction, the repricing of these expectations could drag asset values down faster than any real business crisis.

Musk sells innovation — but some of it is no longer news. Tesla, for example, is losing its uniqueness: in 2025 BYD overtook it in sales (2.26 million versus 1.64 million), and in Q1 2026 their shares were almost equal (13% for Tesla versus 11% for BYD). Musk’s self-driving project is once again delayed: the launch of Full Self-Driving has been pushed to the end of 2026, while Waymo robotaxis had already reached 14 million rides by the end of 2025. Cybertruck is constantly running into problems — from weak sales to serious doubts about the safety of “autopilot”; meanwhile, the Tesla Semi truck has finally entered mass production — with a range of 500 miles and a price of $260–290k, though volumes are still modest (forecast: 5–15 thousand per year). Tesla’s long-term valuation still depends on whether autonomy and robotics move into a viable commercial phase.

Musk’s activity carries political and regulatory risks. Musk’s growing influence in the public sphere increases his dependence on the state as regulator and customer. SpaceX and related projects critically depend on contracts, licenses, and agency decisions. A change in the political climate or stricter regulation could significantly limit the companies’ operational freedom. We already see intensified regulator attention to innovative products — in a case as fresh as the SpaceX IPO, when the U.S. government demanded that Anthropic block foreigners’ access to the latest Fable 5 and Mythos 5 models, citing national security and a discovered “jailbreak” (bypass of protection) — even though Anthropic itself insists the vulnerabilities are minor and inherent to all AI models.

Three Future Scenarios

Musk has created an empire in which resilience depends not only on the brilliance of engineers, but also on the whims of financial markets, political storms, and industrial cycles. Technology here is only half the equation. What future scenarios can be drawn from this?

Optimistic scenario: “Infrastructure for Everything, on Earth and in Space”. In this scenario, SpaceX manages the main trick: after going public, it does not lose momentum, but becomes a global leader in orbital logistics. Starlink becomes the “air” of global communications — invisible, but omnipresent. The Pentagon signs long-term contracts, and defense becomes a reliable financial cushion for Musk. xAI, meanwhile, successfully catches up with the leaders in the race for general-purpose AI, and these developments are built into Tesla’s autopilots and robots. The result: instead of a zoo of startups, there is a coherent technological ecosystem where everything works with everything else.

Base scenario: “Back to Earth”. The hype around AI, robots, and spacecraft gradually cools. Musk keeps promising a colony on Mars, but the timelines keep slipping (a familiar story for him). The companies continue to make money — without panic, but without the previous excitement. Investors no longer pay for the dream, only for the facts. Musk’s empire is still a giant, but it is no longer seen as a miracle — just as a very large, almost standard conglomerate. Multiples cannot rise forever — and that is normal.

Negative scenario: “Breaking Apart”. The tech sector is hit by a crisis — and a global sell-off of “growth stories” begins. Politicians and regulators review contracts and slow down promising directions. At the same time, the Chinese emerge from the shadows and methodically push Tesla out of the electric vehicle market, while Big Tech overtakes xAI in AI models. Then Musk’s ecosystem loses its internal links, assets begin to fall sharply in value — and the dream of a single technological empire collapses into fragments.

***

Regardless of which scenario materializes, what matters more is the very fact of so many different directions being concentrated in one business structure. Markets increasingly assess not current results and the resilience of individual corporations, but the viability of their future scenarios.

Musk has become the most expensive and visible figure in an economy governed by this logic. His valuation is shaped by infrastructure, media, and political expectations, while the boundaries between companies and institutions are becoming less distinct.

The resilience of capital today depends less and less on business stability in the classic sense. For Musk, the ability to keep attention focused on the future is far more important — even if that future is repeatedly delayed.

If you enjoyed this article, consider making a donation — one-time or, even better, monthly. Your support helps us motivate our authors and become better with every article.

Our organization is recognized by the Internal Revenue Service (IRS) as a 501(c)(3) tax-exempt, charitable organization, which means that all contributions made to us are tax-deductible to the fullest extent permitted by U.S. law. Individuals may generally deduct charitable contributions of up to 60% of their Adjusted Gross Income (AGI) for cash donations made to qualifying 501(c)(3) organizations. For donations of appreciated assets (such as stocks or other long-term capital assets), the deduction is typically limited to 30% of AGI, based on the fair market value of the asset. C-corporations may deduct charitable contributions of up to 10% of their taxable income for donations made to eligible charitable organizations.

By submitting a donation, you confirm that you have read and accept the following documents: Privacy Policy and User Agreement, and also give consent to the processing of your personal data.

If you would like to unsubscribe from a monthly donation, please email us at: [email protected]